The Top Features to Look for in a Secured Credit Card Singapore

The Top Features to Look for in a Secured Credit Card Singapore

Blog Article

Decoding the Process: How Can Discharged Bankrupts Obtain Credit Score Cards?

Navigating the world of charge card applications can be an overwhelming job, particularly for individuals that have been discharged from insolvency. The procedure of rebuilding credit rating post-bankruptcy postures special obstacles, commonly leaving many questioning the feasibility of getting credit history cards once more. However, with the ideal techniques and understanding of the eligibility requirements, released bankrupts can get started on a journey towards financial recuperation and accessibility to credit history. However how precisely can they navigate this intricate procedure and protected credit history cards that can assist in their credit rebuilding trip? Allow's explore the avenues readily available for released bankrupts aiming to reestablish their creditworthiness via charge card alternatives.

Comprehending Bank Card Qualification Standard

One crucial consider charge card eligibility post-bankruptcy is the individual's credit report. Lenders usually consider credit report as an action of an individual's credit reliability. A greater credit rating signals responsible economic behavior and may cause far better charge card options. In addition, demonstrating a steady revenue and work background can positively influence charge card authorization. Lenders look for assurance that the person has the ways to settle any type of credit rating encompassed them.

In addition, individuals should understand the various kinds of debt cards available. Secured bank card, for example, need a cash money deposit as collateral, making them more easily accessible for people with a history of insolvency. By comprehending these eligibility criteria, people can browse the post-bankruptcy debt landscape better and function in the direction of rebuilding their financial standing.

Reconstructing Credit Rating After Personal Bankruptcy

One of the preliminary steps in this process is to get a protected credit score card. Guaranteed credit scores cards call for a money deposit as security, making them a lot more obtainable to individuals with a personal bankruptcy background.

An additional method to rebuild credit score after insolvency is to become a certified individual on someone else's credit scores card (secured credit card singapore). This allows individuals to piggyback off the key cardholder's favorable credit rating, possibly enhancing their own credit history

Constantly making on-time payments for financial debts and expenses is vital in restoring credit history. Payment background is a significant consider figuring out credit report scores, so showing liable financial behavior is important. Furthermore, on a regular basis keeping an eye on credit history reports for errors and errors can aid make sure that the information being reported is correct, further helping in the credit scores rebuilding process.

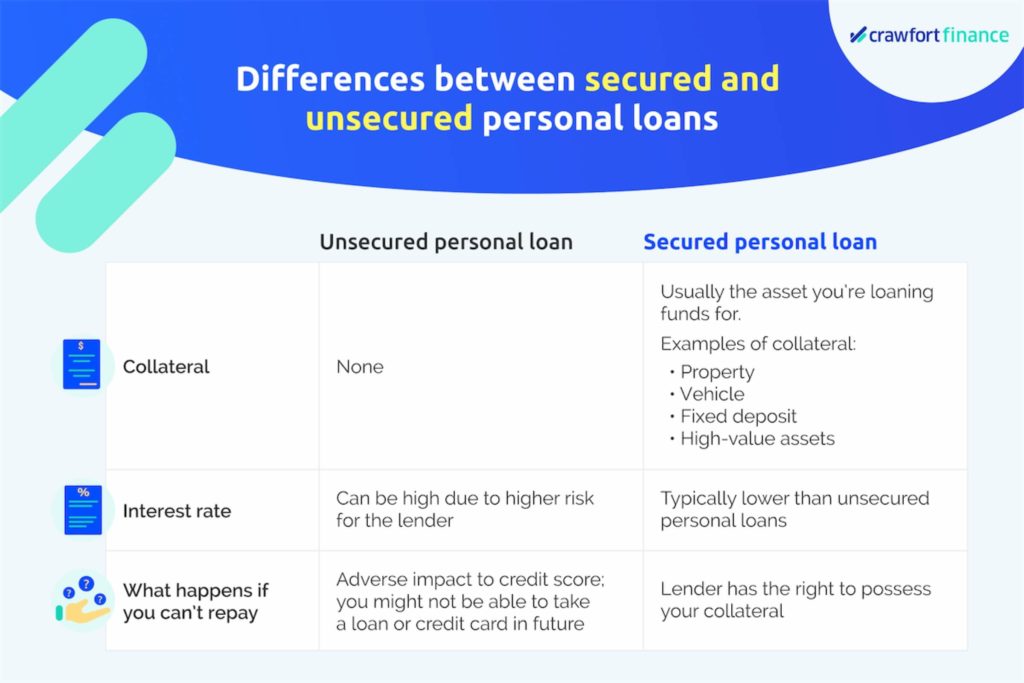

Protected Vs. Unsecured Credit History Cards

When considering credit rating card choices, people might run into the choice in between safeguarded and unsecured bank card. Guaranteed bank card need a cash deposit as collateral, usually equal to the credit line given. This deposit shields the issuer in instance the cardholder defaults on payments. Safe cards are often recommended for people with inadequate or no credit report, as they give a method to develop or rebuild credit rating. On the various other hand, unsafe bank card do not directory call for a down payment and are given based on the cardholder's credit reliability. These cards are a lot more typical and generally included higher credit line and reduced fees compared to safeguarded cards. Nonetheless, people with a background of bankruptcy or bad credit score may find it testing to get approved for unsecured cards. Choosing between secured and unprotected bank card relies on an individual's monetary situation and credit report goals. While secured cards provide a course to improving credit history, unsafe cards supply more read the full info here versatility yet may be harder to obtain for those with a troubled debt history.

Requesting Credit Rating Cards Post-Bankruptcy

Having reviewed the distinctions between safe and unprotected credit score cards, people that have gone through bankruptcy may currently think about the procedure of making an application for credit history cards post-bankruptcy. Restoring credit score after bankruptcy can be challenging, however obtaining a bank card is an essential step towards boosting one's credit reliability. When obtaining credit report cards post-bankruptcy, it is necessary to be strategic and discerning in selecting the appropriate alternatives.

Furthermore, some people may certify for specific unsecured bank card specifically developed for those with a background of personal bankruptcy. These cards may have greater charges or interest rates, but they can still offer a possibility to rebuild credit when used responsibly. Before getting any bank card post-bankruptcy, it is recommended to review the terms and problems meticulously to comprehend the charges, see this page rates of interest, and credit-building potential.

Credit-Boosting Methods for Bankrupts

Restoring creditworthiness post-bankruptcy requires executing effective credit-boosting techniques. For people looking to improve their credit rating after bankruptcy, one vital technique is to acquire a guaranteed charge card. Protected cards need a cash deposit that acts as security, making it possible for people to demonstrate accountable credit usage and payment habits. By making prompt repayments and maintaining credit use low, these individuals can gradually rebuild their credit reliability.

An additional method entails becoming an authorized customer on a person else's credit scores card account. This allows individuals to piggyback off the main account owner's favorable credit report, possibly improving their very own credit history. Nevertheless, it is vital to guarantee that the main account owner keeps good credit habits to maximize the benefits of this method.

Furthermore, continually keeping track of credit history records for errors and contesting any kind of errors can also aid in enhancing credit rating. By remaining positive and disciplined in their credit scores management, people can gradually boost their creditworthiness even after experiencing insolvency.

Verdict

Finally, released bankrupts can obtain bank card by fulfilling eligibility criteria, restoring credit rating, recognizing the difference in between safeguarded and unsecured cards, and applying strategically. By complying with credit-boosting methods, such as keeping and making timely repayments credit scores use low, insolvent individuals can gradually improve their credit reliability and access to credit score cards. It is very important for released bankrupts to be mindful and persistent in their financial behaviors to efficiently browse the process of acquiring charge card after insolvency.

Recognizing the stringent debt card qualification standards is crucial for individuals looking for to obtain credit history cards after bankruptcy. While safeguarded cards offer a course to enhancing credit, unsafe cards offer more versatility yet might be more challenging to obtain for those with a distressed credit history.

In conclusion, released bankrupts can acquire credit cards by meeting eligibility criteria, restoring credit history, comprehending the difference in between protected and unsafe cards, and applying purposefully.

Report this page